Need-Based Financial Aid

For many families, need-based financial aid is essential to making college affordable. But figuring out how to get money for college isn’t simple. With different types of aid, applications, and deadlines to keep track of, the process can feel overwhelming. Still, for families who might not otherwise be able to afford college, it’s well worth the effort.

If you’re not sure how to afford college and are looking for guidance on how to apply for need-based financial aid, this guide is for you! We’ll answer essential questions like:

- How does financial aid work?

- Who qualifies for financial aid?

- What types of aid are available to me?

- Do you have to pay back financial aid?

- What type of loan is based on financial need?

- Where can I find need-based scholarships?

- And more!

We’ll also give an overview of the two most important financial aid applications and highlight common mistakes to avoid throughout the process. But first, let’s start by defining what need-based financial aid actually is.

What is need-based financial aid?

Need-based financial aid is money awarded to students because their family income is not enough to cover the full cost of college. This is different from merit-based aid, which is awarded based on academic performance, talents, and various accomplishments. There are also scholarships that combine both, meaning you need to show financial need and meet other achievement-based requirements.

Families must demonstrate need in order to be offered need-based financial aid. What does demonstrate need mean? In order to demonstrate need, a family must show a gap between what they can feasibly pay, and what the college costs.

Schools will use a numerical figure, the Student Aid Index (SAI) to determine how much need-based aid a family may qualify for. Schools will take a family’s SAI and compare it to their total Cost of Attendance (COA). If a family’s Student Aid Index is less than the Cost of Attendance, the family may qualify for need-based financial aid.

There are different types of financial aid that may be awarded to families that demonstrate need. Need-based scholarships may come from the federal government, local state government, or the school itself. Some private organizations also offer need-based financial aid, so it’s important to apply for need-based aid broadly.

Most need-based financial aid is in the form of grants and scholarships, which do not need to be paid back. While some schools may offer a college student loan, “financial aid” does not automatically mean taking on student debt. In fact, many schools offer financial aid programs that aim to meet 100% of a students’ demonstrated need without loans.

If you’re unsure if your family will qualify for need-based financial aid, the next section will explore how need is calculated.

Who Qualifies — and How Need Is Calculated

How does financial aid work? In order to receive need-based financial aid, you must first qualify. Family income aside, students must generally meet the following criteria for need-based financial aid:

- Be a U.S Citizen or eligible non-citizen (some schools may offer need-based financial aid to international students, however).

- Enrolling in an accredited college or university

- Able to complete a FAFSA

Some families may assume they earn too much income to qualify for financial aid, and never submit an application. You may be leaving money on the table — it’s always worth it to apply just in case.

Student Aid Index

Financial aid is calculated based on an estimated Student Aid Index, or SAI. A family’s SAI is determined by a federal formula that considers a family’s income, assets, household size, and the number of students in college. All of these figures are used together to determine how much a family can feasibly afford each year for college.

Each question on the FAFSA helps calculate a family’s SAI. For example, a family may have a fairly high income, but a large household size and multiple children in college can greatly reduce their SAI. The formula attempts to capture the total amount of expenses families have to manage alongside educational costs.

Once your family’s SAI is determined, colleges will subtract your SAI from the schools’ total cost of attendance to determine the amount of need-based financial aid.

For example, if a family’s SAI totals $10,000 and the cost of attendance is $65,000, this family would qualify for up to $55,000 in need-based financial aid.

In this calculation, total cost of attendance includes tuition, room and board, books, transportation, and personal expenses.

Why Financial Aid Varies by School

While many schools use the federal formula to calculate need-based financial aid, some schools use a different calculation. Financial aid professionals call this “institutional methodology”, as opposed to the “federal methodology” used by the FAFSA.

Many private schools use an institutional methodology to determine a student’s financial need. These schools typically require the CSS Profile in addition to the FAFSA. We’ll cover the major differences between these applications and what you need to know about them later in this guide.

Types of Aid: Grants, Scholarships, Loans, and Work-Study

The different types of financial aid can be confusing to understand. Do you have to pay back financial aid? What is the difference between a grant and scholarship? Which type of loan is based on financial need? We’ve created this chart to help break it all down:

| Aid Type | What is it? | Where does it come from? | Do you pay it back? | Examples |

| Grants | Money you receive that doesn’t need to be paid back, based on financial need | Federal government; state government; colleges | No | Pell Grant (federal) Cal Grant (state of California) Penn Grant (University of Pennsylvania) |

| Scholarships | Money you receive that doesn’t need to be paid back, based on need or merit | Colleges; private organizations | No | Dell Scholars Program QuestBridge National College Match Odyssey Scholarship Program (UChicago) Terry Foundation Scholarship (Texas A&M) |

| Loans | Money you borrow now that must be paid back later with interest | Federal government; private financial institutions | Yes | Federal subsidized loans Federal unsubsidized loans Parent PLUS loans Private student loans |

| Work-Study | Money students can earn by working part-time jobs on campus | Federal government | No | Dining hall worker Administrative aide Research assistant |

Grants and Scholarships

Grants and scholarships are two types of “gift aid”, meaning they do not need to be paid back. Students can apply for federal and school-specific grants and scholarships by completing the FAFSA and CSS Profile.

Eligible students can also apply for additional, private scholarships, sometimes referred to as external scholarships. Most grants and scholarships will be paid directly to a school’s financial aid office to offset your student’s tuition and other college costs.

Loans

College student loans differ greatly from grants and scholarships as they need to be paid back. Loans also accumulate interest, which means the longer you take to repay them, the more money you will owe.

Most student loans are taken out in the student’s name, with a parent sometimes serving as a cosigner. The only exception is the Parent PLUS loan program through the federal government. These loans are held in the parent’s name.

Wondering which type of loan is based on financial need? The answer is, federal subsidized loans. That is because these types of loans do not accrue interest while the student is enrolled in school.

Work-Study

The federal work study program is a need-based program that allows students to work part-time on or off campus, helping them earn money throughout the school year. This funding comes in the form of a paycheck, and is designed to help students manage their personal expenses while in school.

Which type of aid is the best?

While learning how to afford college, it’s also important to recognize that some types of aid are more beneficial than others.

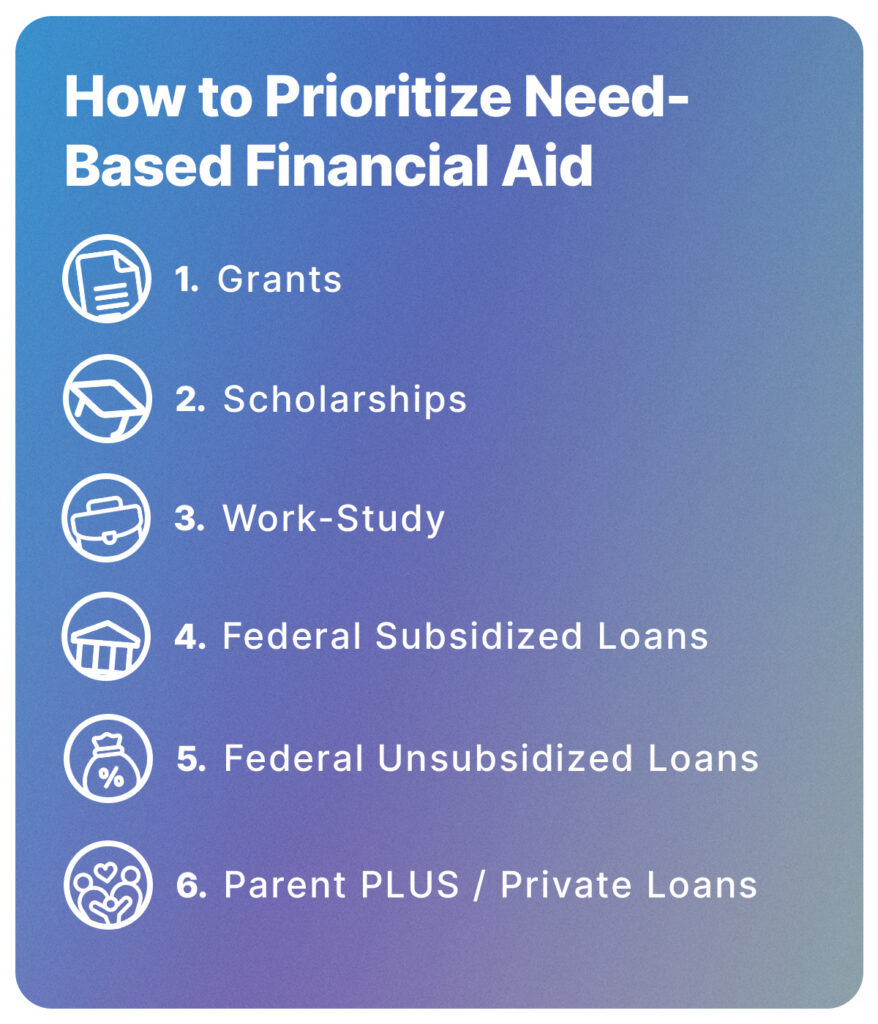

Grants are the best form of need-based financial aid as they are free and solely based on your income and financial situation. Scholarships are also free, though merit-based scholarships can be competitive and may require an extra application. Work study follows as the funds do not need to be repaid. However, students must work in order to earn their funding, which can be challenging to juggle alongside classes and college extracurriculars.

Subsidized loans are placed above other loan programs as they do not accrue interest while a student is enrolled. Unsubsidized loans are considered more favorable than PLUS loans and private loans as the interest rate is typically lower. PLUS loans and private loans sit at the bottom as their interest rates tend to be higher, with stricter repayment options.

When considering loans, it’s important to understand that borrowing money — whether through Parent PLUS loans or student loans — adds financial strain for your family. Before taking on a loan, have an honest conversation with your child about what that student debt will mean in practice, including monthly payments and how long repayment may take. This helps them plan ahead for how they’ll manage and pay off their loans after graduation.

Now that we’ve broken down the different types of financial aid, let’s go over how to apply for financial aid.

The FAFSA: What It Is and How to Complete It

If you’re researching how to get money for college, chances are you’ll come across the FAFSA. The FAFSA, or the Free Application for Federal Student Aid, is the most important financial aid application you’ll need to complete. No matter what types of financial aid you’re looking for, from grants to a college student loan, the FAFSA should be your first step in applying for need-based financial aid.

The FAFSA is the gateway to nearly all forms of need-based financial aid, including federal, state, and college-based aid. It’s important to note that the FAFSA is free. Be wary of websites that require you to pay a fee to file the FAFSA.

In order to file the FAFSA, you will need the following information:

Parent and Student Social Security Numbers

Tax returns (for the 2026-2027 academic year, you’ll need your 2024 tax information)

Records of child support

Current balances of cash, savings, and checking accounts

Net worth of investments

As you apply for need-based financial aid, it’s a good idea for parents and students to complete the FAFSA together. Walking through the form together helps students understand where the different types of financial aid come from, and ensures nothing gets missed or misreported.

The FAFSA will generate an estimated Student Aid Index, which will serve as the basis for need-based financial aid. Be sure to complete your FAFSA early — the application typically opens in October of each year.

The CSS Profile: Do You Need to File It?

The CSS Profile is a secondary financial aid application used by 300+ colleges and universities. It is administered by the College Board, the same organization that administers the SAT. Schools use the CSS Profile to supplement the FAFSA, using the information on the CSS Profile to award institutional need-based financial aid on top of federal aid.

The CSS Profile differs from the FAFSA in a number of ways. The CSS Profile digs a bit deeper into a family’s finances by asking questions about home equity, small business assets, medical expenses, private school tuition paid for siblings, and non-custodial parent income. This is how a single family can see different amounts and types of financial aid between schools.

Some families who may not qualify for federal need-based financial aid can still see significant financial aid awards from CSS Profile schools, as the formula weighs more variables than the FAFSA.

Unlike the FAFSA, the CSS Profile is not free. Families must pay an initial $25 filing fee to a single school, and then an additional $16 for each additional school. However, the CSS Profile will apply a fee waiver if your family income is under $100,000.

If you’re wondering how to afford college for expensive private institutions, the answer is usually by filing the CSS Profile. You can see if a school requires the CSS Profile by checking their financial aid website, or by using the College Board’s official school search tool.

Where to Find Need-Based Scholarships

If you’re wondering about how to pay for college without loans, the answer is: scholarships! Here are a few tips on how to find them.

At many schools, filing the FAFSA/CSS Profile automatically qualifies your student for need-based scholarships. However, be sure to check each school’s financial aid website to see if any scholarships require separate applications, or have specialized deadlines.

When figuring out how to afford college, it’s also worth exploring outside scholarships. You can find need-based scholarships using free online scholarship search engines, such as Fastweb, Scholarships.com, and College Board’s Scholarship Search. Be careful of scholarship search engines that charge a fee, or guarantee an award — these are common scams.

If you’re researching how to get scholarships, remind your student to connect with their guidance counselor. Local employers, religious organizations, and professional associations often offer scholarships to local students that can add up.

Applying to outside scholarships takes time and effort, but it can help your child avoid taking out a college student loan. Since this process is a big part of their future, it’s important for students to take charge. You can help by flagging opportunities you come across, but students should be driving their own process.

Looking for more guidance on how to get scholarships? Check out this guide to winning need- and merit-based scholarships and grants.

Managing Financial Aid Deadlines

Financial aid deadlines may differ from application deadlines, and a missed deadline could mean missing out on need-based financial aid. So, do your research and make note of all financial aid deadlines at each of the schools you plan to apply to.

Both the FAFSA and CSS Profile will typically open on October 1 of each year. It’s a good idea to file these aid applications sooner rather than later, as some need-based financial aid is awarded on a first come, first served basis. Outside scholarships have deadlines scattered throughout the academic year, so it’s important to keep track of these deadlines as they come up.

Creating one, centralized tracker at the start of senior year is a great way to help your student keep on top of all the deadlines they’ll need to manage. Set calendar reminders 2-3 weeks before each deadline, and be sure to save confirmation emails to document which applications you’ve successfully submitted. If your student decides to apply early anywhere, be prepared to file your financial aid applications early as well.

Navigating how to afford college can feel overwhelming, but staying organized and developing a plan can help you keep pace with all the deadlines and requirements.

How to Compare Financial Aid Award Letters

Families who have applied for need-based financial aid will receive a financial aid package from each school their student has been accepted to. You can expect to receive your award letter around the same time or shortly after your child receives their admissions decision.

A financial aid award letter serves as a school’s official offer of aid. The letter will typically break down the different types of financial aid awarded and the total amount of funding offered. Financial aid award letters can differ in format and terminology from school to school, so straight comparisons can be difficult.

How do you know what each college will cost? When reviewing your financial aid award letter, total up the amount of “free money” — the amount of grants and scholarships offered by the school. You’ll want to separate this out from the “self-help” aid, such as student loans and work-study.

To understand how to afford college without taking on debt, you’ll need to determine your family’s real net cost. Your real net cost is the Cost of Attendance minus grants and scholarships, not the total aid package. College student loans eventually need to be repaid, and work study needs to be earned. Focusing on the real net cost will help you decide which college is the best financial fit for you and your family.

It’s also important to understand the terms of the grants and scholarships awarded. Be sure to ask the financial aid office if the financial aid is renewable year to year, if there are GPA requirements that must be met, or if it’s tied to specialized enrollment.

Have more questions? Our guide to Deciphering Your Financial Aid Award Letter has examples and information on accepting your financial aid award.

Appealing financial aid award letters

With many families looking to avoid taking out a college student loan, appealing financial aid award letters has become a common process. If your circumstances have changed since you filed the financial aid applications, it’s a good idea to appeal your financial aid award. Some schools may be able to take the change in circumstances into account and increase your need-based financial aid.

To appeal your financial aid, you’ll likely need to write an appeal letter. This letter should be concise and polite, documenting your change in circumstances or a competitive offer. Be sure to connect with each school’s financial aid office on the best way to submit your appeal letter. For a more detailed explanation of this process, watch this webinar on How to Appeal Financial Aid Awards.

Common Mistakes Parents Make (and How to Avoid Them)

Applying for need-based financial aid is a complex process, and many families unknowingly make mistakes. We’ve compiled the most common mistakes parents make to help you avoid them as you apply for different types of financial aid:

5 Common Need-Based Financial Aid Mistakes

1. Assuming the family earns too much to qualify.

With the rising cost of college, more families are qualifying for financial aid. Don’t make assumptions about your eligibility — the best way to find out if you qualify for financial aid is to apply.

2. Filing the FAFSA late.

Financial aid deadlines matter, and delaying your FAFSA can lead to missing out on grants and scholarships. File as early as you can to make sure you’re not missing out on any funds to help cover your costs.

3. Not filling out the CSS Profile.

Some families assume they only need to file the FAFSA. However, many schools use the CSS Profile for institutional scholarships. Double check each school your student is applying to and read their financial aid requirements. Keep track of which schools require the CSS Profile and which do not.

4. Accepting loans without reading the terms.

While many families are navigating how to pay for college without loans, they are a common form of financial aid. However, it’s important to fully understand the terms and conditions of college student loans before taking them. This will prevent any surprises and help minimize financial hardships down the line.

5. Ruling out private colleges based on sticker price.

It may be intimidating to apply to schools that cost $70,000+ per year, however, many private colleges offer robust need-based financial aid. Don’t rule out a specific school based solely on the sticker price. Research their need-based aid programs and see what a more realistic price may be based on your income.

Need-Based Financial Aid – Final Thoughts

From grants and scholarships to student loans and work study, learning how to apply for financial aid comes with a lot of complex questions. Understanding the different types of financial aid, how aid is calculated, and how to manage the financial aid process is critical to ensuring you get the best possible aid package.

Keep on top of your FAFSA and CSS Profile submissions, and make sure you’re meeting all posted financial aid deadlines. Start the process early — many families need time to collect all the financial information the applications require.

If you’re still not sure how to afford college for your student, CollegeAdvisor is here to help! We help families explore and apply for need-based financial aid so they can make their college dreams a reality.

This article was written by Jessica Klein. Looking for more admissions support? Click here to schedule a free meeting with one of our Admissions Specialists. During your meeting, our team will discuss your profile and help you find targeted ways to increase your admissions odds at top schools. We’ll also answer any questions and discuss how CollegeAdvisor.com can support you in the college application process.